The stablecoin market changed today. Visa, Stripe, Mastercard, and 145 other institutions announced Open Standard and Open USD (OUSD), a joint stablecoin consortium that represents the most significant development in digital payments since the GENIUS Act was signed into law. This is not a crypto story. This is a financial infrastructure story, and every bank and credit union executive in the country should understand what happened.

This post breaks it down: what Open USD is, why it matters, what the economics mean, and what community and regional financial institutions need to do right now.

What Is Open USD and Open Standard?

Open Standard is a new open infrastructure initiative for stablecoin-based payments and financial activity. Open USD is the stablecoin issued through that infrastructure, designed to help businesses move value at scale while supporting broad participation and collaborative governance.

The consortium behind it is led by Visa and includes Stripe and Mastercard, with Coinbase also participating. Zach Abrams, CEO of Bridge which was acquired by Stripe in 2025 for >$1b, is interim CEO. BlackRock and BNY hold the reserves. The economic model: 100% yield pass-through to end users, with a basis point toll per transaction. Over 100 distribution partners were signed before the first coin was minted. Each partner receives the same terms, ensuring an even playing field.

This has serious institutional backing, serious distribution, and a serious economic model.

The Stablecoin Market Before Today

To understand why this matters, you need to understand the market it is entering.

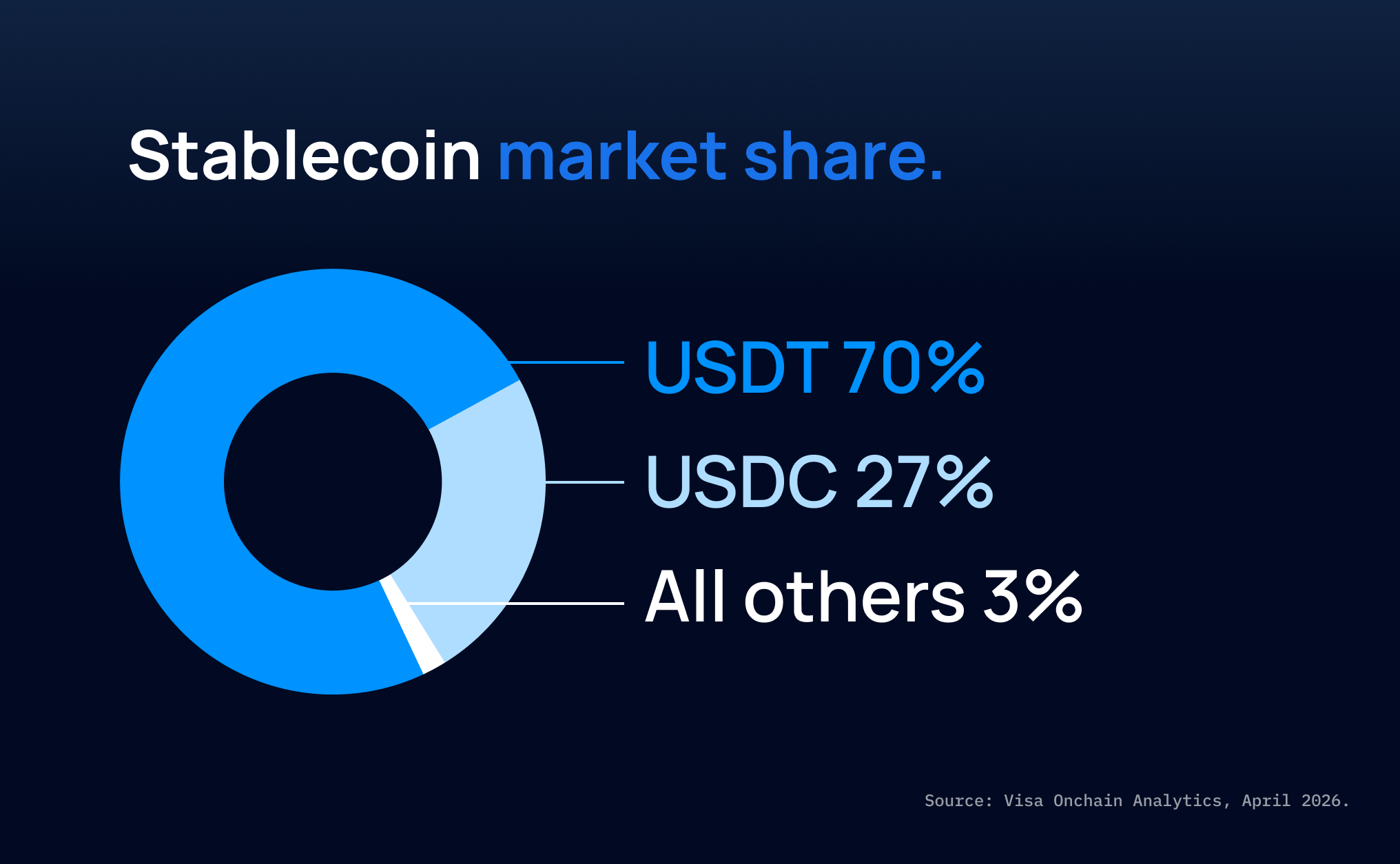

The stablecoin market currently sits at roughly $278 billion, according to Visa's own on-chain analytics data. But despite that scale, the market has been extraordinarily concentrated. Tether's USDT ($195B) and Circle's USDC ($75B) together account for nearly 97% of all stablecoins in circulation. Dozens of stablecoins from fintechs, neobanks, and crypto-native companies collectively represent just 3% of the market.

That concentration persisted for a simple reason: stablecoin scale requires massive distribution and network effects. It is not enough to issue a technically sound stablecoin. You need to be where the money already moves.

How Visa, Stripe, and Mastercard Got Here

None of this came out of nowhere. Each member of the consortium spent the past two years making strategic acquisitions and infrastructure investments specifically to reach this moment.

Mastercard announced in March 2026 the acquisition of BVNK, a stablecoin infrastructure company that processes $30 billion in annual transaction volume, for up to $1.8 billion. It is the largest stablecoin infrastructure deal on record, eclipsing every prior acquisition in the space.

Stripe paid $1.1 billion for Bridge in 2024 and acquired Privy in 2025. Bridge provides stablecoin payment orchestration infrastructure, and Stripe has used it to open stablecoin accounts in 110 countries. Stripe has consistently made the right moves in this space.

Visa expanded its stablecoin-linked settlement network to 9 blockchains and is now running at a $7 billion annualized settlement rate, up 50% in a single quarter. The company has been quietly building the rails that would make a consortium like this possible.

Why Open USD Changes the Game

The GENIUS Act, signed into law in July 2025, formally defines these instruments as payment stablecoins. The name is not incidental. Payment stablecoins are primarily for payments … not yield, not savings, not speculation. They are the digital equivalent of a wire transfer that settles instantly, 24 hours a day, seven days a week, anywhere in the world.

Given that definition, the strategic logic of Open USD is obvious: why would the largest payment networks in the world move trillions of dollars on someone else's stablecoin? The answer is they would not. Open USD is Visa, Stripe, and Mastercard building the coin they will actually use, and the coin they want merchants, businesses, and financial institutions to use alongside them.

This is the first serious challenger to USDC's position as the dominant GENIUS Act-compliant stablecoin. Circle built USDC into a $75 billion asset. But Circle does not have Visa's merchant network, Stripe's developer ecosystem, or Mastercard's institutional relationships. Open USD does.

The Network Effects Are Accelerating Everywhere

The Open USD announcement did not happen in a vacuum. Across the U.S. and globally, every major consumer-facing financial network has been moving aggressively into stablecoins in 2026. The velocity is higher than almost anyone predicted.

Western Union launched USDPT on Solana, issued by Anchorage Digital Bank and backed 1:1 by USD reserves, to bypass SWIFT for real-time global settlement. Bybit is already integrated as a partner exchange. A self-custody wallet and payment card called Stable by Western Union is coming next.

MoneyGram launched MGUSD in June to power its own global remittance network, putting stablecoin infrastructure at the core of one of the world's largest money transfer operations.

Zelle unveiled ZelleUSD and is expanding internationally, extending the most widely adopted domestic bank payment network into the stablecoin ecosystem.

Cash App rolled out stablecoins to all customers, putting stablecoin access in front of tens of millions of users who may not identify as crypto users at all.

PayPal expanded PYUSD to 70 global markets in March 2026 and rolled it out across Venmo. Per Visa's own on-chain data, PYUSD now sits at $3.38 billion in circulation, making it the sixth-largest stablecoin in the world.

SoFi launched SoFiUSD in May, becoming the first U.S. national bank to issue a stablecoin and make it available directly in a banking app. SoFiUSD is live for nearly 15 million members on Ethereum and Solana.

Taken together, over 100 million U.S. consumers now have access to stablecoins through apps they already use every day. This is not adoption coming. This is adoption here.

A Parallel Race: Tokenized Deposits

Stablecoins are not the only digital money story. A parallel and related race is playing out in tokenized deposits — digital representations of bank deposits settled on-chain.

On June 5, 2026, The Clearing House announced that 17 major banks will build a tokenized deposit settlement network targeting a 2027 launch. The participating institutions are: JPMorgan, Bank of America, Citigroup, Wells Fargo, HSBC, PNC, Truist, U.S. Bank, TD Bank, BNY, BMO, Citizens Financial Group, Fifth Third, KeyBank, Regions Financial, Santander, and Huntington National Bank.

The platform will enable on-chain clearing and settlement of tokenized deposits with programmable payment controls, linking to The Clearing House's existing CHIPS and RTP rails. The primary initial use case is large multinational corporate treasury operations.

Competing efforts include the Cari Network (Gene Ludwig), FIS Constellation (Jon Eisenstein), the Hazel Network in Texas (Jeff Sinnott and Shawn Main of Vantage Bank, and Caitlin Long of Custodia Bank), and JPMorgan's own Kinexys platform.

Stablecoins and tokenized deposits are at different points of maturity. Stablecoins have demonstrated clear product-market fit. They grew to hundreds of billions in circulation outside of the traditional banking system, settling globally without reserve accounts at central banks. That non-reserve settlement is their structural advantage. It is what makes them fast, cheap, and globally interoperable.

Tokenized deposits, by design, stay inside the banking system. They are bank liabilities on a chain. Whether they achieve comparable adoption and liquidity to stablecoins over other real-time payment rails is an open question, and one that Stablecore is actively helping banks and credit unions think through.

What This Means for Banks and Credit Unions

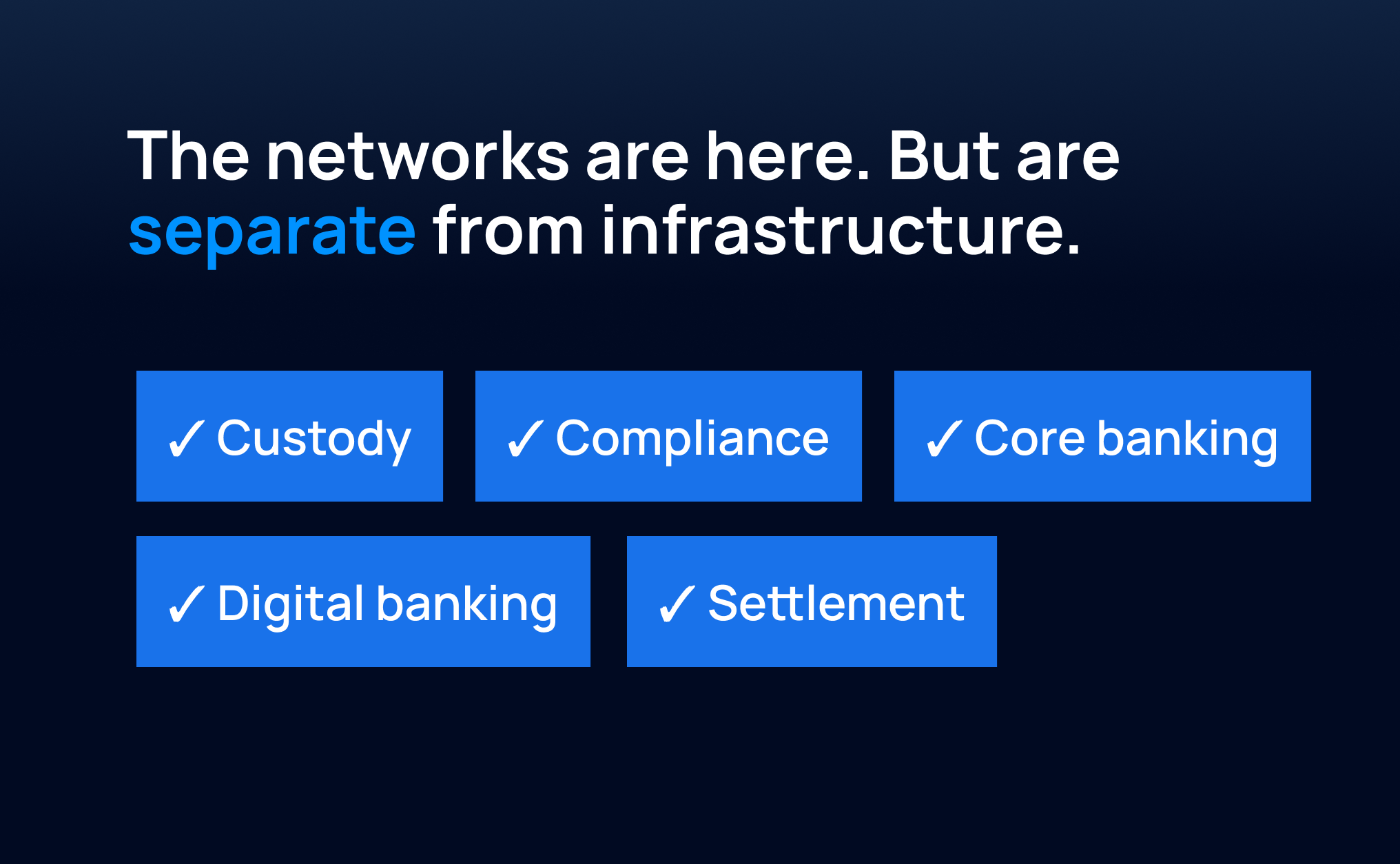

Here is the most important thing to understand: the networks are not the infrastructure.

To participate in any of these networks and offer stablecoin products to your members or customers, to settle on-chain, to earn yield on digital assets, a financial institution needs its own foundational infrastructure in place first.

That infrastructure has five components:

Custody: Who holds the digital assets? How are private keys secured? What are the regulatory requirements for custody at your charter type?

Core banking integration: How does stablecoin activity flow into your existing core? How are balances, transactions, and interest treated on your ledger?

Digital banking: How does your member or customer access, view, and transact with digital assets in your app or online banking?

Compliance: What are your BSA/AML obligations for stablecoin transactions? How do you handle travel rule requirements, OFAC screening, and enhanced due diligence?

Settlement: How do you connect to on-chain settlement networks and bridge between on-chain activity and your existing payment rails?

The institutions that are building this infrastructure now will be positioned to participate as the networks mature. The reason there are not more US banks - and no credit unions - in the Open USD announcement is that very few have the capabilities to participate today.

The data from 2026 is clear: customers and members are accessing stablecoins through Zelle, Cash App, PayPal, Venmo, and other apps regardless of whether their primary financial institution offers digital assets. The question for community and regional banks and credit unions is not whether digital assets are coming. The question is whether your institution is the one offering them.

Stablecore's View

At Stablecore, we have been asked many times to help financial institutions build proprietary stablecoins or tokenized deposit networks. Our answer has been consistent: it requires enormous volume, network effects, and distribution to compete at scale in the stablecoin market. Visa, Stripe, and Mastercard have all three.

What most community and regional financial institutions need is not a proprietary stablecoin — it is the infrastructure to connect to the stablecoins and digital asset networks that already exist and are growing rapidly. That is what we build.

We expect to see meaningful consolidation among financial institutions that are not positioned for the digital asset era. We also expect to see significant winners — institutions that moved early on infrastructure, built the integration layer, and became the trusted digital asset partner for their members and customers.

Open USD and the broader developments of June 30, 2026 accelerate that timeline. The window to build is open now.

About Us:

Stablecore is the platform enabling community and regional banks and credit unions to offer stablecoins, tokenized deposits, and digital asset products. Learn more at stablecore.com.

External sources:

Visa Onchain Analytics: visaonchainanalytics.com/supply

Mastercard/BVNK: CNBC, March 17, 2026

TCH announcement: PR Newswire, June 5, 2026

SoFiUSD: SoFi investor relations, May 27, 2026

PayPal PYUSD 70 markets: PayPal newsroom, March 17, 2026

MoneyGram MGUSD: PR Newswire, June 2, 2026